Did you know that when it comes to saving for retirement, more and more people are choosing a Self Invested Personal Pension (SIPP)? Yes, it’s true and if your goals are similar to ours, a SIPP is going to be a great way to help you achieve them.

Did you know that when it comes to saving for retirement, more and more people are choosing a Self Invested Personal Pension (SIPP)? Yes, it’s true and if your goals are similar to ours, a SIPP is going to be a great way to help you achieve them.

Surprisingly, SIPPs were created in 1989, yet it is only in the last five years or so that they have become popular and are now the preferred way for smart investors to manage their pension arrangements.

In this series of posts we'll take a look at SIPPs in more detail and explore how they work.

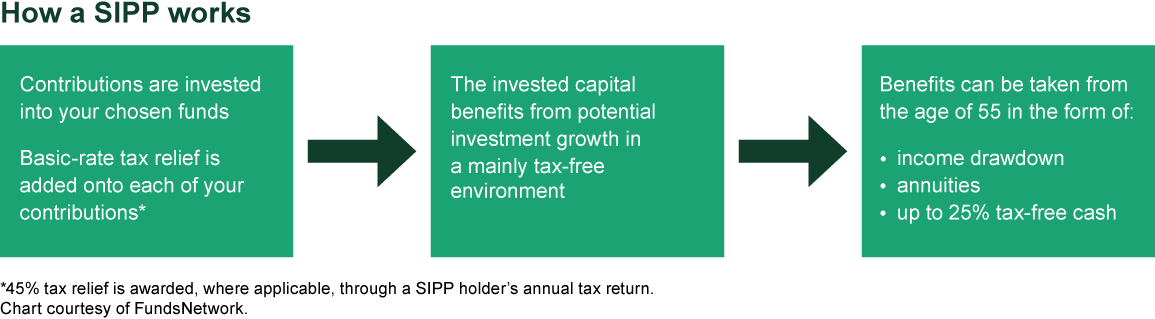

How a SIPP works

The chart below shows how a SIPP works.

What are the advantages of a SIPP

The four main advantages of a SIPP are:

- Tax efficiency

- Greater choice

- Better planning

- You can open a SIPP for a child.

In this post we'll look at the first of these, the tax efficiency of a SIPP.

SIPP tax advantages

A SIPP is a long-term savings vehicle with great tax advantages and from the age of 55, you can receive up to 25% of your pension fund value as a tax-free lump sum (subject to certain limits). The remaining benefits can be taken gradually as an income or as additional lump sums, both of which are subject to your tax rate at that time.

Contributions into a SIPP offer significant tax benefits. Most importantly, you can claim tax relief on your contributions. This means that if you are a basic rate taxpayer, the Government will add another 20p into your pension for every 80p you pay in. Your contribution allowance is £50,000 but this amount will be reduced from £50,000 a year to £40,000, with effect from April 6th 2014.

You will only receive tax relief on 100% of your relevant UK earnings if these are less than £50,000 per year. If you are taking advantage of an additional ‘carried forward’ allowance, tax relief will also be claimed on these contributions up to a maximum of £50,000 per contribution period.

If you pay tax at a higher or additional rate, you can continue to claim any additional tax relief on the contributions made by you or by a third party on your behalf through your self assessment return on contributions up to the stated limits. Any contributions made to your SIPP after the age of 75 will not be entitled to any tax relief.

If you work for a company that contributes to your pension, make the note that employer contributions are not eligible for tax relief. In the March 2012 budget, the Chancellor of the Exchequer proposed a change to the additional rate of tax from 50% to 45% for the tax year 2013/14 and this will affect the amount of pension tax relief that can be claimed if you are a high earner.

He also announced in his 2012 Autumn Statement that the maximum amount an individual could save into their pension during their lifetime and receive tax relief would be cut from £1.5 million to £1.25 million as from April 6th 2014. This is called the ‘lifetime allowance’. The lifetime allowance is the maximum amount of pension saving you can build up over your life that benefits from tax relief. If you build up pension savings worth more than the lifetime allowance you'll pay a tax charge on the excess.

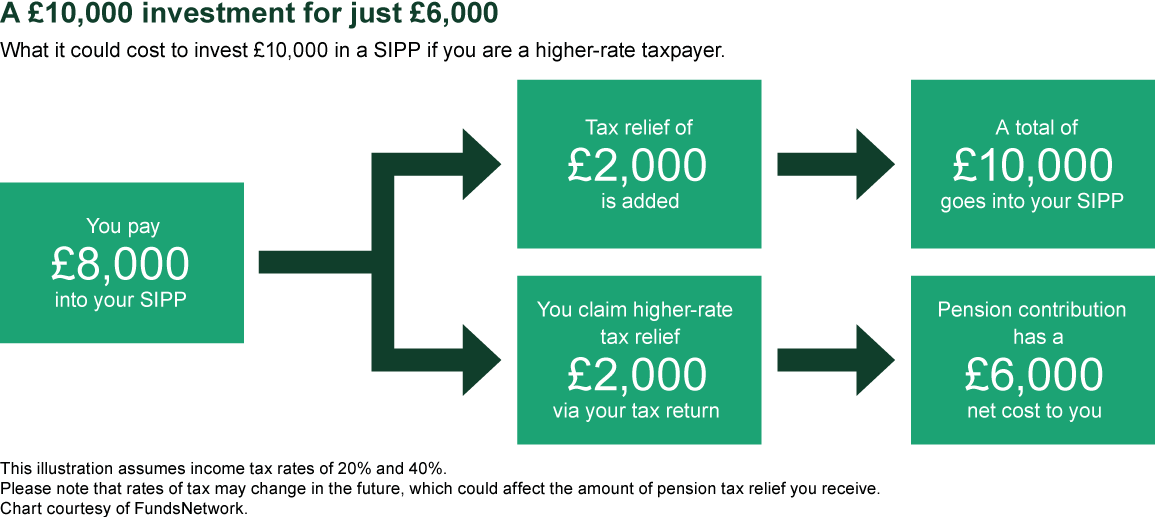

A £10,000 investment for just £6,000

The chart below shows how a £10,000 investment in a SIPP would only cost you £6,000 if you are a higher-rate taxpayer.

SIPP tax advantages - the key points

- For every 80p you pay into your pension – the Government adds another 20p.

- Most SIPP providers will invest this tax relief immediately

- If you’re a higher rate taxpayer, you may claim up to a further 20p for every £1.

- Your SIPP investments will grow free of tax.

- The contribution allowance for the 2013/2014 tax year is £50,000.

- You will only receive tax relief of up to 100% of your relevant UK earnings.

- You can transfer from other pensions and investments into your SIPP

- You may take up to 25% of your SIPP as a tax-free cash lump sum after age 55.

Your money will grow much faster

UK pension fund investments grow free of income tax and capital gains tax (CGT), which allows funds to grow your money faster than taxed alternatives and benefit considerably over the longer term due to the effects of compounding.

As always, if you have any questions or thoughts on the points covered in this post, please leave a comment below or connect with us @ISACO_ on Twitter.

About ISACO

ISACO is a specialist in ISA and SIPP Investment and the pioneer of ‘Shadow Investment’, a simple way to grow your ISA and SIPP. Together with our clients, we have £57 million actively invested in ISAs and pensions*.

Our personal investment service allows you to look over our shoulder and buy into exactly the same funds as we are buying. These are investment funds that we personally own and so you can be assured that they are good quality. We are proud to say that by ‘shadowing’ us, our clients have made an annual return of 12.5% per year over the last four years** versus the FTSE 100’s 7.4%.

We currently have close to 400 carefully selected clients. Most of them have over £100,000 actively invested and the majority are DIY investors such as business owners, self-employed professionals and corporate executives. We also have clients from the financial services sector such as IFAs, wealth managers and fund managers. ISACO Ltd is authorised and regulated by the Financial Conduct Authority (FCA). Our firm reference number is 525147.

* 15th November 2012: Internal estimation of total ISA and pension assets owned by ISACO Investment Team and ISACO premium clients.

** 31st December 2008 - 31st December 2012.

ISACO investment performance verified by Independent Executives Ltd.

To download our free report 'A Golden Opportunity' >>

To download our Shadow Investment brochure >>

To start your 14 day free 'no obligation' trial of Shadow Investment >>