Here's your chance to read some content taken from our brand new SIPP Guide. The good news is that the content includes all the new 'pension freedom' rules explained to you in plain English. Enjoy!

This information is taken from ISACO’s brand new SIPP Guide, to download your free copy, click here.

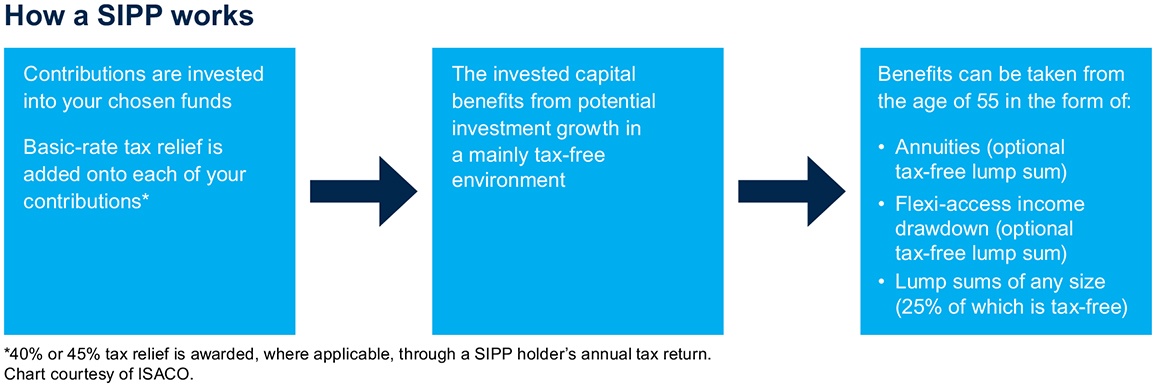

How a SIPP works

A SIPP is not an investment itself but simply a tax wrapper that protects the investment from personal liability for tax. Please note however that unlike ISAs, when you eventually start to take an income from your SIPP, the income taken will be taxable. Let’s take a look at how a SIPP works.

What are the advantages?

The four main advantages of a SIPP are:

- Tax efficiency

- Greater choice

- Better planning

- You can open a SIPP for a child

Tax efficiency

A SIPP is a long-term savings vehicle with great tax advantages – tax relief on contributions, tax-free growth of the fund and some of the benefits are tax-free when you draw them too. For example, from the age of 55, you can receive up to 25% of your pension fund value as a tax-free lump sum (subject to certain limits). The remaining fund used to have to be used to provide you with a taxable income, but recent changes have given much greater flexibility as to how you access the remainder of your pension pot.

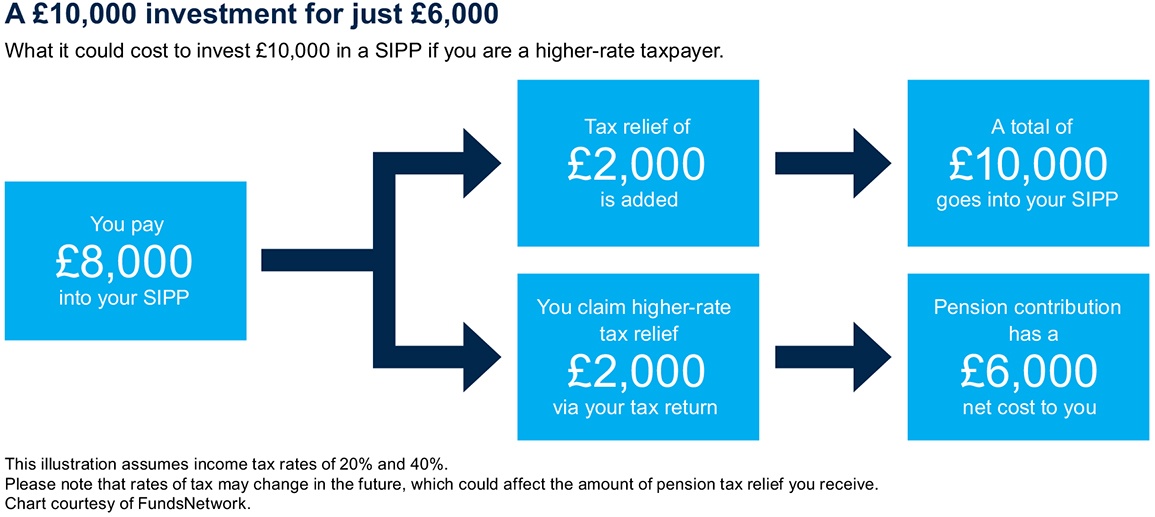

Contributions into an HMRC registered pension such as a SIPP offer significant tax benefits - most importantly you can claim tax relief on your contributions. This means that for every £1.00 that goes into their SIPP a basic rate income tax payer only pays 80p – the other 20p comes from the government in the form of tax relief. It is even better for higher rate taxpayers who get 40p tax relief, and additional rate taxpayers get 45p tax relief, on every £1.00 contribution to a SIPP. Higher and additional rate taxpayers will claim their additional tax relief (i.e. the excess over the basic rate) through their annual self-assessment return. The diagram below illustrates how tax relief works for a higher rate taxpayer.

Your maximum annual tax relievable contribution is limited to £40,000. You can contribute more than this each year to a SIPP but the contribution will not get tax relief. Contributions made after you reach age 75 will not get tax relief either.

If your relevant UK earnings (basically your income from employment or self-employment) are less than £40,000 per year then your maximum tax relievable SIPP contribution is 100% of these earnings rather than £40,000.

Even if you have no relevant earnings at all you can contribute up to £3,600 a year (gross) into a pension and receive basic rate tax relief.

If you are taking advantage of an additional ‘carried forward’ allowance, tax relief will also be claimed on these contributions, up to a maximum of £50,000 per contribution period.

The amount of pension savings you can build up over your life that benefit from tax relief is subject to an overall maximum – this is called the ‘lifetime allowance’. If you build up pension savings worth more than the lifetime allowance you’ll pay a tax charge on the excess. For the 2015-16 tax year the lifetime allowance is £1.25 million.

SIPP key points

- For every 80p you pay into your pension the Government adds another 20p in tax relief – SIPP providers will invest this tax relief some 2–6 weeks after your payment is made

- If you’re a higher rate taxpayer, you may claim up to a further 20p for every £1 you contribute to your SIPP

- If you’re an additional rate income taxpayer, you may claim up to a further 25p for every £1 you contribute to your SIPP

- Your SIPP investments will grow free of tax*

- The maximum tax relievable contribution allowance for the 2015-16 tax year is £40,000

- You will only receive tax relief on contributions up to 100% of your relevant UK earnings if these are less than £40,000

- You can transfer from other pensions and investments into your SIPP

- You may take up to 25% of your SIPP fund as a tax-free cash lump sum after age 55 (this is expected to rise to 57 in 2028)

How to grow your money much faster

UK pension fund investments grow free of income tax and capital gains tax (CGT), which allows funds to grow your money faster than taxed alternatives and benefit considerably over the longer term due to the effects of compounding.

* When we talk about pension funds growing tax-free you should be aware that pension funds cannot reclaim the 10% tax credit on UK share dividends.

Greater Choice

SIPPs allow you to choose where you want to invest your pension savings. Instead of being restricted to a limited range of funds – as with some other types of pension – SIPPs offer a wide range of investments to choose from. You can also decide how much you want to invest and how often. You can even transfer in pension plans from other providers.

You can typically choose from thousands of funds run by top managers, as well as pick individual shares, bonds, gilts, unit trusts, investment trusts, exchange traded funds (ETFs), cash and commercial property (but not residential property). The precise range of investment options open to you will depend on which SIPP manager you select.

With a SIPP you are free to invest in:

- Cash & Deposit accounts (in any currency, providing they are with a UK deposit taker)

- Insurance company funds

- UK gilts

- UK shares (including shares listed on the Alternative Investment Market)

- US and European shares (stocks and shares quoted on a recognised stock exchange)

- Unquoted shares

- Corporate Bonds

- Permanent Interest Bearing Shares

- Commercial property

- Unit trusts

- Open ended investment companies (OEICs)

- Investment trusts

- Traded endowment policies

- Futures and options

- Exchange Traded Funds (ETFs)

This information is taken from ISACO’s brand new SIPP Guide, to download your free copy, click here.

As always, if you have any questions or thoughts on the points covered in this post, please leave a comment below or connect with us @ISACO_ on Twitter.

As we grow our wealth, you grow yours. Together we prosper.

ISACO are a specialist in ISA and SIPP investment and together with our clients have an estimated £75 million actively invested1. To help investors like you, we offer a high end service called ‘Shadow Investment’. Put simply, we invest and you invest beside us. As we grow our wealth, you grow yours.

How does Shadow Investment work?

Shadow Investment allows you to look over our shoulder and buy the same investments that we are buying. It’s an intensely personal service which gives you the opportunity to piggyback on our expertise and makes investing easier, simpler and much more enjoyable.

Delivering superior performance

We have an active investment strategy which aims to control risk and deliver superior performance. Over the last 17 years2, we’ve beaten the FTSE 100 by 77.9% and over the last 3 years3, we’ve made an average annual return of 9.5% versus the FTSE 100’s 5.7%.

Get in touch

If you have over £250,000 actively invested, click here to arrange a free financial review (valued at £495) with Paul Sutherland, ISACO’s Managing Director.

1 Internal estimation taken January 1st 2015 of total ISA and pension assets owned by the ISACO Investment Team and ISACO premium clients.2 December 31st 1997 - December 31st 2014 ISACO 105.5%, FTSE 100 27.6%.

3 December 31st 2011 – December 31st 2014.

ISACO investment performance verified by Independent Executives Ltd.