Here's your chance to read some content taken from our brand new SIPP Guide. The good news is that the content includes all the new 'pension freedom' rules explained to you in plain English. Enjoy!

Here's your chance to read some content taken from our brand new SIPP Guide. The good news is that the content includes all the new 'pension freedom' rules explained to you in plain English. Enjoy!

This information is taken from ISACO’s brand new SIPP Guide, to download your free copy, click here.

Better planning

A person retiring 20 years ago had very little choice as to how they could use their pension pot other than to buy an annuity. Over the intervening years a wider range of options were gradually introduced but each of these still included restrictions on how a pension pot could be accessed and used.

The introduction of George Osbourne’s Pension Freedoms though, from the start of the 2015/16 tax year, has fundamentally changed the choices people face when they reach retirement. On one hand it has given people much more flexibility as to how they generate an income in retirement but on the other it has made the choice more complex.

To help make decisions at retirement, anyone over 50 can receive free impartial guidance under the Pension Wise scheme set up by the government (www.pensionwise.gov.uk) although this is quite basic so if your pension arrangements are complex, or your pension pot is large, then you would benefit from seeing an Independent Financial Adviser (IFA) as well.

It is important to understand that these new freedoms generally apply to money purchase pension schemes only - in other words schemes where you build up your own pension pot. They do not apply to final salary occupational pension schemes. You should also be aware that your current pension provider may not offer all of the options discussed below but that it may be possible to transfer your fund to a provider who does.

You may well have heard a lot about these Pension Freedoms in the press but what options will you have and what will they mean for you?

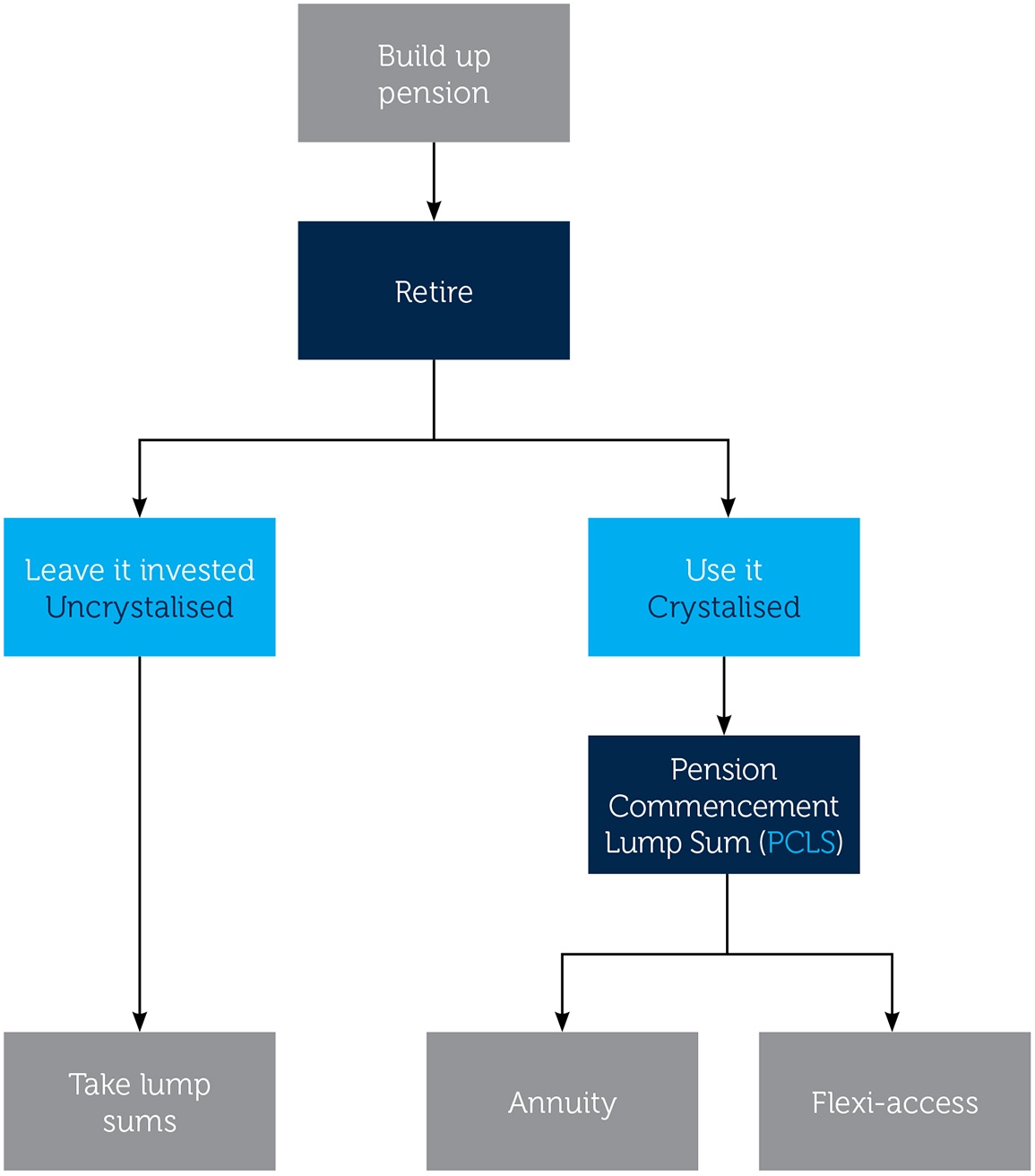

When can I access my pension funds?

You can decide to access your pension pot at any time after you reach the age of 55 (age 57 from 2028), but you should remember that the aim of a pension is to provide for you for the rest of your life. The earlier you access it, the longer it has to last and the less time it has to grow.

How can I use my pension pot when I decide to retire?

A person deciding to retire in the future has three basic options as to how they can use their pension pot.

- Withdraw lump sums

- Invest it in an annuity

- Place it in a flexi-access drawdown pension scheme

However, the first financial decision you will need to make on reaching retirement is whether you want to access your pension pot at all.

If you have enough income without dipping into your pension pot then you should consider leaving it untouched and even continuing to make contributions – remember, you can get tax relief on contributions until you reach age 75. This would mean that your fund would continue to grow in the tax advantageous environment, and make use of the wide range of investment options a SIPP offers.

As you can see, one of the options is only available to you where you have left the funds invested so let’s start by looking at that.

Option 1: Withdraw lump sums

This option allows you to withdraw lump sums of any size from your ‘uncrystallised’ pension fund. (Uncrystallised funds are those which haven’t been used already to buy an annuity or been allocated into a flexi-access pension or income drawdown scheme). Hence you may also see these referred to as Uncrystallised Funds Pension Lump Sums (UFPLS).

Each of the UFPLSs you take will be 25% tax-free but the remainder will be added onto any other income for the year and the total of this amount will be then liable to income tax at the appropriate rate.

This could be a good option if you require a large lump sum – you could even withdraw your whole pension fund in this way if you wished. However, it needs very careful planning to ensure that you do not end up paying income tax unnecessarily when you make a large withdrawal this way.

It is also important to understand that you cannot take a tax-free lump sum using this option – each UFPLS is 25% tax-free and 75% taxable. The tax-free lump sum (known as the Pension Commencement Lump Sum or PCLS) can only be taken when you crystallise your pension fund. This happens when you use your pension fund to purchase an annuity or allocate it to a flexi-access pension, so let’s look at those options now.

Option 2: Invest it in an annuity

An annuity converts your pension pot into a guaranteed income for life so this is a particularly attractive option for people who want to be sure that their money will not run out. The major downside though is that once the annuity has been purchased the pension pot has gone and you no longer have access to your funds. The government is considering changing this to allow people to cash in an annuity but that is not possible at present.

Annuities are offered by insurance companies and the amount of income they produce will depend on how long the insurer expects a person to live. This means that older people, and those whose life expectancy may be reduced by a health condition, will receive a higher income.

A person purchasing an annuity has various options. You can choose for the income paid to:

- be at a level amount every year

- increase each year, either by a fixed percentage or in line with inflation

- decrease, so as to pay out a larger amount in the early years of retirement when the person is able to be more active

- be guaranteed for a fixed number of years so it will continue to pay out even if the purchaser dies

It is also possible to buy a capital protected (or value protected) annuity. This will provide a return of any unpaid income as a lump sum on the annuitant’s death.

If your pension has been set up through an insurance company you can still choose to buy your annuity through a provider of your choice using the Open Market Option (OMO). Everyone purchasing an annuity should use the OMO to ensure that they get the annuity that will pay the highest income for their particular circumstances.

The income provided by an annuity will all be liable to income tax. If you want to take advantage of the PCLS (the tax-free lump sum) you would arrange this at the time you purchase the annuity. So, for example, if a person had a pension pot of £1m and they wanted to take the maximum PCLS they would receive a tax-free lump sum of £250,000 (i.e. 25% of £1m) and the remaining £750,000 would be used to purchase the annuity.

Option 3: Place it in a flexi-access drawdown pension scheme

If you decide to allocate your pension pot to a flexi-access drawdown (FAD) pension you are able to take a Pension Commencement Lump Sum and take a regular income just as with an annuity. The income you could receive from a FAD though is much more flexible. Under this option your pension pot remains invested and part of it is drawn down on a regular basis to provide an income. The amount and frequency of the payment is up to you but the whole of each income payment will be liable to income tax.

The risk with a FAD is that if your pension investments do not perform as well as expected then the income taken may have to be reduced. There is even the chance that the person runs out of money entirely.

Prior to the 2015/16 tax year there were two other ways in which a person could draw down income from their pension pot – flexible drawdown and capped drawdown. Those on a flexible drawdown scheme were automatically transferred across to a FAD as these two schemes were very similar. Those on capped arrangements (which restricted the amount a person could drawdown based on their age) had a choice as to whether they transferred to a FAD or stayed in a capped scheme.

The Money Purchase Annual Allowance (MPAA)

One other point to consider when thinking about options at retirement is whether you want to continue making contributions to a pension scheme. The maximum a person may be able to contribute to a pension scheme and receive tax relief is normally £40,000 a year – the annual allowance.

Where a person has taken advantage of one of the flexible options though (such as a UPLS or entering a FAD) then a lower maximum of £10,000 a year usually applies – this is known as the Money Purchase Annual Allowance (MPAA).

So which option should I choose?

Each of the three options we have outlined has advantages and disadvantages so it is very important to think carefully about them to ensure that you end up with a solution that matches your needs and your attitude to risk.

One great thing about the pension freedoms though is that you don’t have to make just one choice – you can mix the options up to suit your needs. Let’s consider an example. David has reached age 62 and has decided that he wants to gradually retire - he has a pension fund worth £1,020,000. He decides that he wants to make some changes to his house and take a long holiday with his partner.

In order to fund this he takes an Uncrystallised Pension Funds Lump Sum of £120,000. Part of this UPFLS is tax-free (25% - £30,000) and the remainder is liable to income tax. He leaves the remaining pension pot of £900,000 invested in his SIPP.

He works for another two years part time and is able to cope comfortably on his income from his employment. At age 64 he decides he wants to stop working and retire. By this time his SIPP fund has grown to £1m.

David now decides to use half of his pension pot to buy an annuity and attribute the other half to a flexi-access drawdown scheme. As both these options crystallise his pension pot he can take a Pension Commencement Lump Sum. He decides to take the maximum PCLS of £250,000 (ie. 25% of his £1m crystallised pension pot).

Of the remaining £750,000, half is used to purchase an annuity which will provide him with an income for life. The other half is attributed to a flexi-access drawdown scheme which David can use to provide him with an additional income which he will be able to increase or decrease as his needs demand.

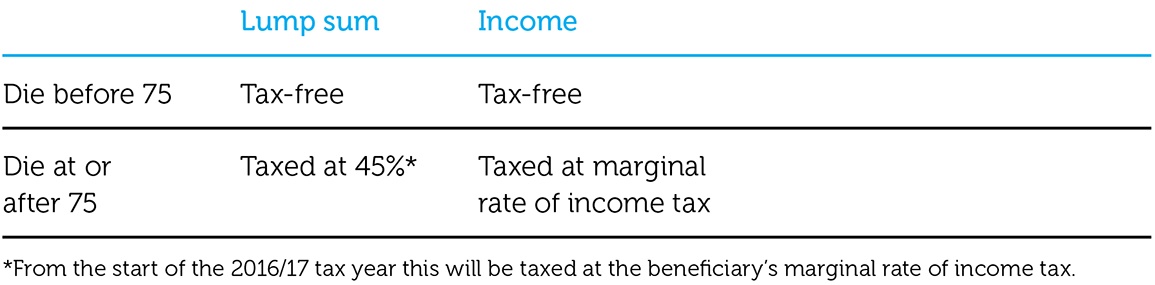

What happens to your pension fund if you die?

When a person dies it may be possible for them to pass their pension onto anyone who they name as a beneficiary. Since the Pension Freedoms were introduced, how these pension benefits are taxed when they are passed on now largely depends on whether or not the person died before they reached the age of 75.

Under certain circumstances there may be an additional tax charge if the pension fund of the person who has died exceeded the lifetime allowance (currently set at £1.25m) or if benefits are not taken from the pension fund within two years of the person’s death.

If there is any of the pension fund remaining when the beneficiary dies then they can nominate a further beneficiary to pass the fund onto and it would again be liable to tax in a similar way to that described in the table above.

Where the person has purchased an annuity before they die then any lump sum or income benefits a beneficiary receives will be liable to tax in the same way as we have described above. It is important to remember though that an annuity will simply stop paying out on the annuitant’s death unless they have made specific choices when they bought it – for instance a guaranteed period or a level of capital protection.

Regardless of the age of the person when they die, or the type of pension they are passing on, the pension fund will not be liable to inheritance tax.

This information is taken from ISACO’s brand new SIPP Guide, to download your free copy, click here.

As always, if you have any questions or thoughts on the points covered in this post, please leave a comment below or connect with us @ISACO_ on Twitter.

As we grow our wealth, you grow yours. Together we prosper.

ISACO are a specialist in ISA and SIPP investment and together with our clients have an estimated £75 million actively invested1. To help investors like you, we offer a high end service called ‘Shadow Investment’. Put simply, we invest and you invest beside us. As we grow our wealth, you grow yours.

How does Shadow Investment work?

Shadow Investment allows you to look over our shoulder and buy the same investments that we are buying. It’s an intensely personal service which gives you the opportunity to piggyback on our expertise and makes investing easier, simpler and much more enjoyable.

Delivering superior performance

We have an active investment strategy which aims to control risk and deliver superior performance. Over the last 17 years2, we’ve beaten the FTSE 100 by 77.9% and over the last 3 years3, we’ve made an average annual return of 9.5% versus the FTSE 100’s 5.7%.

Get in touch

If you have over £250,000 actively invested, click here to arrange a free financial review (valued at £495) with Paul Sutherland, ISACO’s Managing Director.

1 Internal estimation taken January 1st 2015 of total ISA and pension assets owned by the ISACO Investment Team and ISACO premium clients.2 December 31st 1997 - December 31st 2014 ISACO 105.5%, FTSE 100 27.6%.

3 December 31st 2011 – December 31st 2014.

ISACO investment performance verified by Independent Executives Ltd.